Find Out More

Where has the demand gone?

The elasticity of our inelastic demand

Tough Season

2019 offered up one of the most challenging production environments we’ve seen in a long time. However, the grain markets were equally as tough, with high market volatility throughout the season. This caused some financial heartache amongst the export/trading community, meaning 2019 will be a year to forget for both growers and buyers alike. One of the reasons (amongst others) that led to our prices coming off significantly was a result of our perceived inelastic export demand proving its elasticity. In WA and SA, prices at harvest time were very strong, incentivising growers to sell, however the international wheat market was also high. This meant the premium for Aussie wheat versus other exporters (namely Black Sea) delivered into South East Asia (SEA) wasn’t that high, at around US$15-20/t. In the past, this level of premium would incentivise flour millers in SEA to buy Australian origin, with the additional cost being justified by the superior milling qualities of our wheat versus others.

Curve Ball

However, it became apparent in the first couple of months of this year that this ‘inelastic demand’ that Australian exporters were banking on was much more elastic than first thought. Indonesia has been the biggest buyer of Australian wheat every year since 2003. At the start of the year, it was a foregone conclusion that they would continue this winning streak. The general consensus in the market at the time was that Indonesia’s demand requirements for Australian wheat would bottom out between 1.5-2mmt. However, as the chart illustrates, Indonesia was able to switch from using Australian origin wheat, cutting their Aussie imports to their lowest level in over 20 years, importing less than 1mmt. This is because the premium we’ve charged in the past, is no longer possible in the current environment. Tess Walch in her article about the rise of Argentinian exports sums it up as ‘dollars are speaking louder than quality’ referring to Indonesia’s willingness to switch away from our relatively expensive wheat into cheaper sources, despite the lower quality finished product. Outside of not wanting to pay a premium price and the extremely competitive milling market in SEA, the severe droughts we’ve suffered domestically have also done us no favours. Our production variability is making it hard for international consumers to consistently rely on Aussie wheat. For example, within 24 months, Australia went from a record 33Mt wheat crop, down to 17Mt (almost a 50% drop!). At the same time our export competition is churning out consistently large crops that global importers are gorging on.

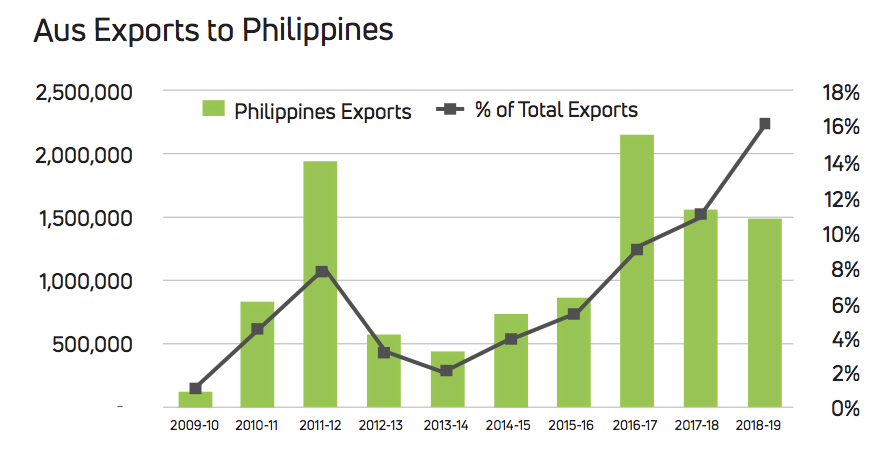

No Longer a Premium

It’s unlikely Australia will again be able to charge such a premium into these markets and achieve the level of exports we need each season. This is not to say there is no premium for Aussie wheat, it’s just closer to US$5/t now, so we’re more or less competing head to head with other exporters and hoping for vessel freight to rally in order to maximise our geographical advantage. One quiver in our bow is the Philippines, who were our biggest buyer in 2018/19. They have been consistently increasing their share of Aussie exports over the past decade. This is partly due to an advantageous tariff exemption that Australian wheat enjoys over our competitors. This 7% tariff exemption allows us to price a premium versus other feed exporters, but still win the business if our premium is within 7% of other offers. Looking towards 2019/20, the market here will be less willing to pay up for wheat in export zones (WA/SA) if the premium into the world market is too high, as our once strong inelastic import customers have voted with their feet towards our cheaper competitors.

Author: Andrew Retallick, Senior Commodity Adviser, Market Check