Find Out More

The Future of the Grain Industry

The Road is Rarely Straight

Industry Leaders & Losers

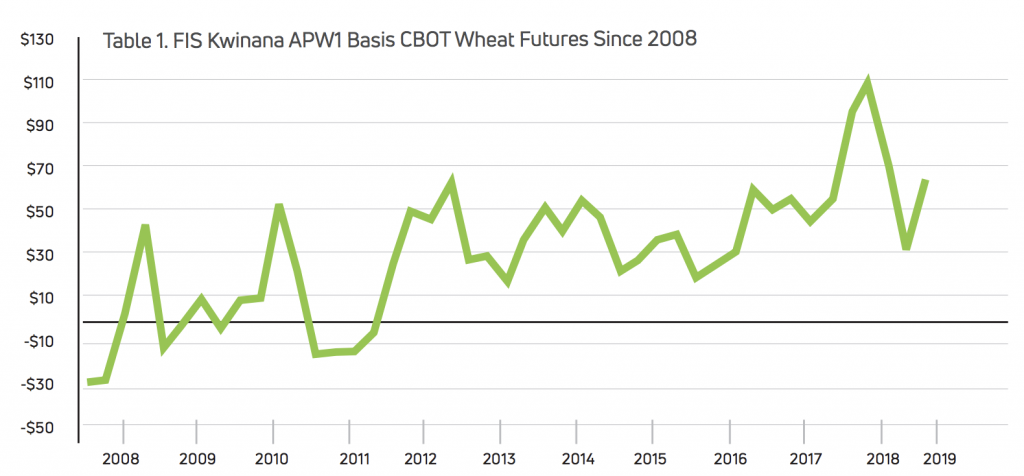

The Australian grains industry has gone through significant change since I started my career in 2005 and I’ve witnessed much of this change first hand through the lens of various supply chain participants. Australian growers have experienced big swings in market participants, demand dynamics, prices, weather and production. The market witnessed a period of expansion for the first 7 to 8 years post deregulation in 2008 as new entrants vied for market share. During this period, strong competition saw increased liquidity throughout the domestic and export markets, leading to higher volatility and stronger relative prices for growers (see figure 1). But following consecutive years of losses, the grains industry began a contractionary period. The industry is still going through this uncomfortable phase which involves the consolidation and/or complete exit of some industry participants. Inefficient supply chain structures such as expensive ‘take or pay’ contracts, changing global demand dynamics and volatile production and prices in Australia have all been contributing factors. But a lack of foresight and willingness to collaborate may have also been at fault. Some had a mandate or strategy to control as much of the supply chain as possible and were thus tied to volume instead of value and suffered as a result. This culminated in trading and marketing losses for grain exporters, based on publicly available reports of over $500 million during the 2014/15 season and another $500 million last financial year. These exporters provide a valuable service to the supply chain and although the biggest beneficiary of these losses has been Australian growers, it’s not sustainable and we’re already witnessing a smaller demand pool as a result. As the grains industry continues to consolidate, Australian growers will be forced to carry more of the year-round grain price risk – especially post-harvest.

On the other hand, many industry participants have flourished in their respective areas, focusing on adding value in specific areas of the supply chain. These industry participants vary across different regions and include storage providers, logistical operators, grain marketing advisers, exporters, domestic consumers and brokers. Based on my experience, those participants that have excelled tend to focus on a specific area of the supply chain and/or region, honing their skillset over time and providing a specialised service that is creating value. Consider McDonalds focusing on developing a home delivery application rather than focusing their efforts on collaborating with the experts in that field, such as Uber Eats. This is illustrated through McDonalds ongoing experimentation with ‘Ghost Kitchens’, which remove the need for seating and front-of-house staff by shifting focus entirely to delivery and take-out food. They have also recently announced their collaboration with Uber to allow food to be delivered by drone, with first deliveries set to commence later this year in San Diego. [1] Industry leaders focus on their strengths and areas of the industry they know best, then collaborate with experts in other fields to further benefit the customer and grow their businesses.

On the other hand, many industry participants have flourished in their respective areas, focusing on adding value in specific areas of the supply chain. These industry participants vary across different regions and include storage providers, logistical operators, grain marketing advisers, exporters, domestic consumers and brokers. Based on my experience, those participants that have excelled tend to focus on a specific area of the supply chain and/or region, honing their skillset over time and providing a specialised service that is creating value. Consider McDonalds focusing on developing a home delivery application rather than focusing their efforts on collaborating with the experts in that field, such as Uber Eats. This is illustrated through McDonalds ongoing experimentation with ‘Ghost Kitchens’, which remove the need for seating and front-of-house staff by shifting focus entirely to delivery and take-out food. They have also recently announced their collaboration with Uber to allow food to be delivered by drone, with first deliveries set to commence later this year in San Diego. [1] Industry leaders focus on their strengths and areas of the industry they know best, then collaborate with experts in other fields to further benefit the customer and grow their businesses.

The Future Looks Bright

Despite recent adverse weather conditions, industry contraction and changing demand dynamics tempering some enthusiasm for the future, the prize for Australian grain producers remains huge. There has been a tremendous interest in investing in Australian farmland, particularly in the last couple of years. [2] This isn’t surprising given ABARES reported in 2016 that large family broad-acre farms were achieving operating rates of return on capital close to 5.5% per annum excluding capital appreciation. For example, if you include capital appreciation of 6.6% over the last 24 years in Victoria, [3] the combined return on capital is quite attractive. The macroeconomic outlook moving forward for the demand for Australian grains, pulses and oilseeds also remains positive. Projections issued by Economic and Social Affairs of the United Nations puts the world population at approximately 9 billion people by 2050, a 25% increase of current levels. Asia is forecast to remain the most populous region by 2030 and of the next billion people to move into the middle class, 88% are expected to be in Asia, largely supported by a minimum annual growth of 6% in China and India. [4] As a result of the growth in both population and the middle-class economy, countries such as China and India are projected to support global demand for agricultural products such as wheat. [5] Over 80% of Australian grain exports head to Asia, and Australia has an impressive track record for pursuing trade liberalisation and brokering preferential trade deals in key export markets with a number of free trade agreements (FTA) secured in recent years. [6]

There is concern over the short-term growth of Asian markets due to the US-China trade dispute and its effects on exports and business investment. The September 2019 ABARES Economic Outlook stated one of the concerns for Australia is the deceleration in consumption growth in year-on-year terms in some of its key agricultural export markets, including South Korea, Hong Kong, Singapore, Taiwan, Thailand and Malaysia. “However, domestic economic conditions remain reasonably robust in the less trade-exposed economies of Indonesia and the Philippines, and in Vietnam, which has benefited from a diversion in trade from China.” [7]

The demographics and geographical advantage in Asia, where living standards and incomes are shifting, should see a dramatic increase in the demand for Australia’s agricultural exports. This potential rise in the future demand for Australian grains, pulses and oilseeds must be met with innovative solutions and collaboration to extract maximum value along the supply chain. These innovative solutions will likely revolve around more efficient logistics infrastructure, improved data analytics, collaborative execution models and more valuable and informed grain marketing decisions from growers. Collaboration along the whole supply chain by various participants who excel in their various fields from the exporter down to the grower will unlock value and ultimately increase farm-gate returns.

Learning from the Past

Making decisions in hindsight is a luxury we don’t have, but learning from the past and making better decisions in the future is how we will succeed as an industry. I’ve recently completed reading a book by Ray Dalio called ‘Principles’ and learnt a lot about the power of reflecting and learning from mistakes. Ray Dalio is the founder of the world’s largest hedge fund, ‘Bridgewater Associates’, and predicted the global financial crisis of 2007. Interestingly, he played a role in designing a poultry-related futures strategy that allowed McDonald’s to launch the Chicken McNugget. “Everyone makes mistakes. The main difference is that successful people learn from them and unsuccessful people don’t.” [8] So, what can we learn from the past and what can we do to win in the future? We know the inefficiencies in the supply chain are becoming less of an issue and the market is acting more rationally, no longer are we going to witness exporters elevating grain onto a vessel at a negative $20 per tonne margin or more. We also know that Australian grain prices are strongly linked to the global market. Looking at figure 2, Asian imports of wheat since 2008 have changed, we no longer have captured ‘inelastic’ demand into Asian destinations.

Australian grain imports are now also a reality, as of the 30th August 2019, “6 permits to import around 360,000 tonnes of high-protein Canadian milling wheat have been issued.” [9] Another 14 import permits are being assessed for the importation of canola, corn, wheat and grain sorghum from the USA and Canada in 2020. Therefore, we need to be monitoring multiple pricing points and understanding what they mean to make better grain marketing decisions. Our cash prices compared to global benchmarks must be monitored and tracked. Growers cannot look at cash prices or ‘deciles’ in isolation, as they don’t give a complete picture of how under or overvalued our grain prices are.

This was proven last harvest when ASX wheat prices hit $185 per tonne over CBOT wheat futures. Growers who had forward sold in 2018 based on deciles instead of hedging, left up to $140 per tonne on the table.

Consolidation has not only been happening at the exporter level, but at the grower level too. In August 2019, ABARES reported that from 2000-01 to 2017-18, the total number of Australian grain farms fell by around 34%. They also reported that the number of farms planting more than 2,400 hectares of grain increased, with these farms increasingly dominating the total production of grains, oilseeds or pulses. [10] This is consistent with our own membership base, with the average size of our long-term clients increasing overtime. What we witness at Market Check is that many of our long-term clients, who have been growing in size, are constantly adopting more innovative approaches to important areas of their farming businesses. Areas such as precision agriculture and improved farming practises, adoption of new breeding technologies, utilisation of cloud-based systems, geospatial data collection, financial management, improved logistical processes and grain marketing have seen big improvements. The area we focus on at Market Check is grain marketing, and we’ve seen strong net returns for our Members since deregulation in 2008 (+8.6% PA) through the adoption of our year-round grain price risk management approach that monitors both domestic and global pricing indicators. Compound these annual returns over 10 years and it’s easy to see why these Members are growing their farming enterprises for generations to come.

Droughts and Round-Abouts

This extended drought market has taken a considerable toll, both financially and emotionally on Australian farmers, regional townships and the service providers that support them. Whether you accept climate change is real or not, the Bureau of Meteorology’s ‘State of the Climate Report’ released last year stated the frequency of extreme heat events has increased. There has also been an approximate 11% decline in April to October rainfall in the southeast and southwest of Australia since the late 1990s. [11] The volatility in annual weather and therefore production and prices doesn’t seem to be going away. The good news is that we know it is cyclical and the round-about will swing back around sooner or later, albeit with a few less passengers.

Those that recognise their strengths and are willing to collaborate with the experts in their field will succeed in a future that looks bright. We’ve witnessed it with grain marketing and it will become a bigger focus as the market continues to contract and the grower is expected to manage more of the year-round grain price risk. As the grains industry continues to contract leading to fewer players and weaker competition for grain, growers will need to rely more heavily on external grain marketing advisers who are the experts in their field if average operating returns are to remain strong. Using 12.1% average farmland returns in Victoria [3] combined with Market Check’s 8.6% year-round strategy returns per annum, Australian growers are really outperforming most widely accepted benchmarks. [4]

The future does look bright, but there is a need to continue to look inwardly, understand the reality of the industry and learn, so we can adapt, survive and thrive. As Ray Dalio says, “remember to reflect when you experience pain,” those that will succeed will do so by learning from tough market environments, focusing on strengths, outsourcing and/or collaborating weaknesses and adapting to win in the future.

Editor: Richard Perkins, Market Check

Image credit: Chris Watson (Farmpix)

References

[1] Carson, B. (2019) Forbes (Online) First Look: Uber Unveils New Design For Uber Eats Delivery Drone. Published Oct 28, 2019. https://bit.ly/2Wy4X5T

[2] Hendy, S. (2016) Colliers International. Research and Forecast Report: Australian and New Zealand Rural Agribusiness, Ripe for the picking, A new dawn for agribusiness.

[3] Rural Bank. (2019) Australian Farmland Values Report: Victoria. https://bit.ly/2WujY8Q

[4] Kharas, H. (2018) Global Economy & Development Working Paper. The unprecedented expansion of the global middle class. An update.

[5] Johnson, S. (2017). IBIS World Industry Report A0149. Grain Growing in Australia. June 2017

[6] KPMG. (2018) KPMG, March 2018 – Discussion Paper. McCormick, D. (2015) Select Asset Management Australia. Exploring agriculture investment.

[7] ABARES. (2019) Economic Outlook; Agricultural Commodities. Published September 2019.

[8] Dalio, R. (2017) Principles: Life and Work. ISBN: 9781501124020

[9] Brown, A. (2019) ABARES Wheat: September quarter 2019

[10] ABARES. (2019) ABARES. Grain Farms based on annual Australian Agricultural and Grazing Industries Survey. Published Aug 12, 2019 https://bit.ly/338T3C8

[11] Bureau of Meteorology/CSIRO. (2018) State of the Climate 2018. https://bit.ly/2JBHzPM